Electrolux 2019

In 2019, Electrolux strengthened its platform for future growth by launching important new product ranges, initiating additional efficiency measures and investing in modularized products in automated manufacturing.

This Annual review covers the consumer business following the decision by the Board in 2019 to propose to distribute the business area Professional Product (Electrolux Professional) as a separate company.

Key highlights 2019

- Sales growth of -1.3% (1.2).

- Operating margin excluding non-recurring items of 3.8% (4.8).

- Lower volumes and manufacturing transition costs in North America impacted earnings negatively.

- Major product launches contributed to continued mix improvements.

- Increased prices fully offset significant headwinds from raw material costs, trade tariffs and currency.

- Comprehensive manufacturing consolidation projects and global streamlining measures initiated.

Electrolux in 2019

Sales growth for continuing operations, excluding currency translation effects was -1.3%. Lower volumes, particularily in North America impacted sales in 2019. While new product launches and mix improvements contributed to sales. Divestments impacted sales by -0.3%.

Operating margin excluding non-recurring items for continuing operations was 3.8%. Lower volumes and manufacturing transition costs in North America impacted earnings negatively. Mix improvements across business areas contributed and price increases offset higher costs for raw materials, trade tariffs and currency headwinds.

Operating cash flow after investments for the Group, including Electrolux Professional, amounted to SEK 3.4bn. Good contribution from operating cash flow, while higher investments had a negative impact. Aquisitions impacted cash flow negatively by SEK 467m.

Key figures 20191)

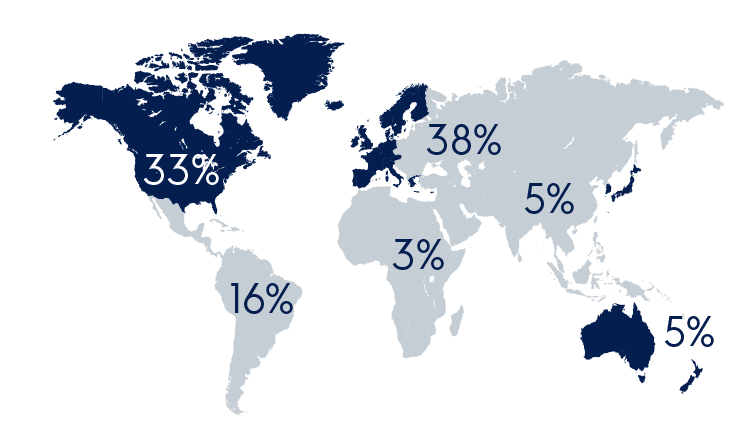

Sales by region

Core markets

Growth markets

1) Key figures refer to the consumer business, exclusive of business area Professional Products.

Targets

The Electrolux Group's financial targets contribute to maintaining and strengthening the company's leading, global position in the industry and generate a healthy total return for Electrolux shareholders.

An average annual total return of approximately 7%. Over the past ten years, Electrolux shareholders have received an average annual total return of approximately 7%. The Group’s capacity to create healthy cash flow and to enhance operational efficiency plays a major role in contributing to this value creation. There is further potential for profitability by increasing margins.

Outstanding consumer experiences contributes to higher profitability. Based on the strategic framework, innovative products for outstanding consumer experiences are to contribute to higher profitability and a margin of at least 6%. A capital turnover-rate of at least 4 times combined with an operating margin of at least 6% should yield a minimum return on net assets of 20%.

Continued profitable growth Further potential for value creation is possible if Electrolux can increase sales and improve its profitability level. The business has to achieve a sustainable profitability level before further investments are made in targeted profitable growth. The objective is an average annual sales growth of at least 4%.

For more information on the Electrolux business model and path to profitable growth, see Strategy.

2019 execution

1) Financial targets are for continuing operations, exclusive of Electrolux Professional, over a business cycle

2) Engagement index

3) Halving the climate impact, million tonne's CO2, by 2020 relative to 2005 levels

Celebrating a century of better living

Electrolux turned 100 years old in 2019 and can be proud of its achievements over the past century

Better Living Program

Electrolux celebrated its anniversary year by launching the Better Living Program – a bold initiative to enable it to continue to be at the forefront of sustainability

Seperation of business area Professional Products

Electrolux has a long track record of value creation by successfully distributing operations to shareholders as new listed companies

Looking for PDFs and reports?

![]()

Electrolux

Electrolux is a leading global appliance company that has shaped living for the better for more than 100 years. We reinvent taste, care and wellbeing experiences for millions of people around the world, always striving to be at the forefront of sustainability in society through our solutions and operations. Under our brands, including Electrolux, AEG and Frigidaire, we sell approximately 60 million household products in approximately 120 markets every year. In 2019 Electrolux had sales of SEK 119 billion and employed 49,000 people around the world.

S:t Göransgatan 143

SE-105 45 Stockholm, Sweden