The Electrolux Control System (ECS) has been developed to ensure accurate and reliable financial reporting and preparation of financial statements in accordance with applicable laws and regulations, generally accepted accounting principles and other requirements for listed companies. ECS adds value through clarified roles and responsibilities, improved process efficiency, increased risk awareness and improved decision support.

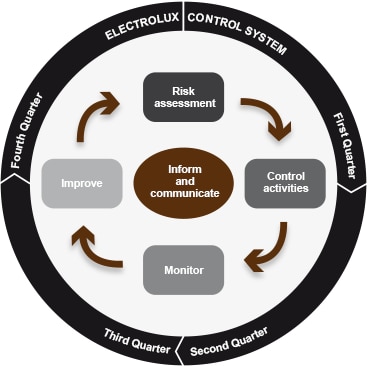

ECS is based on the framework for internal control issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). The five components of this framework are control environment, risk assessment, control activities, monitor and improve and inform and communicate.

Control environment

The foundation for the Electrolux Control System is the control environment, which determines the individual and collective behavior within the Group. It is defined by policies and procedures, manuals, and codes, and enforced by the organizational structure of Electrolux with clear responsibility and authority based on collective values.

The Electrolux Board has overall responsibility for establishing an effective system of internal control. Responsibility for maintaining effective internal controls is delegated to the President. The governance structure of the Group is described in the first section of the Corporate governance report 2012. Specifically for financial reporting, the Board has established an Audit Committee, which assists in overseeing relevant manuals, policies and important accounting principles applied by the Group.

The limits of responsibilities and authorities are given in instructions for delegation of authority, manuals, policies and procedures, and codes, including the Electrolux Code of Ethics, the Electrolux Workplace Code of Conduct, and the Electrolux Policy on Corruption and Bribery, as well as in policies for information, finance and credit, and in the accounting manual. Together with laws and external regulations, these internal guidelines form the control environment and all Electrolux employees are held accountable for compliance.

Responsibility for internal control is defined in the Electrolux Internal Control Policy. All entities within the Electrolux Group must maintain adequate internal controls. As a minimum requirement, control activities should address key risks identified within the Group. Group Management have the ultimate responsibility for internal controls within their areas of responsibility. Group Management is described in the Presentation of Group Management.

The Electrolux Control System Program Office, a department within the Internal Audit function, has developed the methodology and yearly time plan for maintaining the Electrolux Control System. To ensure timely completion of these activities, specific roles aligned with the company structure, with clear responsibilities regarding internal control, have been assigned within the Group, see table Electrolux Control System – Roles and responsibilities.

Over the last years, training and support have been provided to the thousands of persons with assigned ECS roles globally. The objective of the training has been to educate in risk and internal control and provide hands-on tools and techniques in order to effectively carry out the assigned responsibilities. These training sessions have been a mix of regional training sessions, computer-based training modules and net meetings.

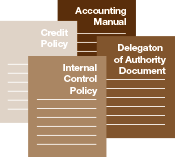

Control environment — Example trade receivables

Accounting Manual

Rules for revenue recognition and calculation of provision for doubtful trade receivables.

Credit Policy

Rules for customer assessment and credit risk that clarify responsibilities and are the framework for credit decisions.

Delegation of Authority Document

Details the approval rights, with monetary, volume or other appropriate limits, e.g., approval of credit limits and credit notes.

Internal Control Policy

Details responsibility for internal controls. Controls should address the Minimum Internal Control Requirements (MICR) within every applicable process, for example "Order to Cash".